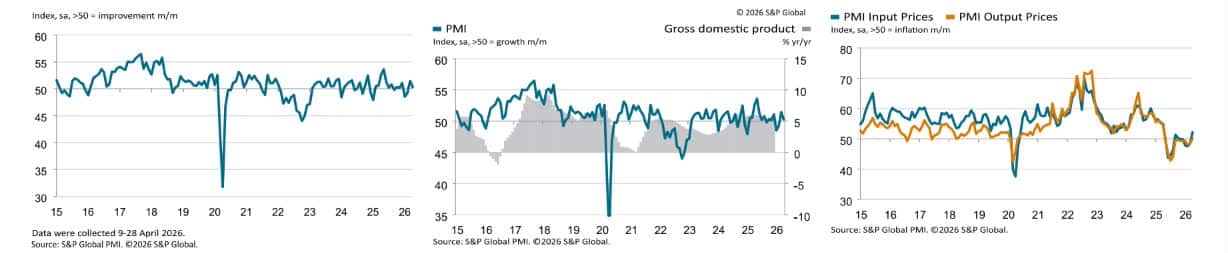

The S&P Global Ghana Purchasing Managers’ Index (PMI) posted 50.3 in April 2026, down from 51.4 in March, as private-sector output fell for the third time in four months. New orders continued to rise, but renewed input-cost pressure from higher fuel prices and imported items dragged business activity lower.

What The PMI Shows

- Headline PMI: 50.3 in April (vs 51.4 in March)

- Above 50 = expansion, below 50 = contraction

- Reading is the weakest expansion in several months

- Output decreased for the third time in the past four months, albeit only marginally

The Drivers

- New orders kept rising — demand is still there

- Input costs increased for the first time in six months, breaking a long disinflation streak

- Higher fuel prices and imported item costs were the headline factors

- Some respondents directly blamed rising prices for the activity slowdown

Why It Matters

- PMI is one of the cleanest near-real-time signals of Ghanaian private-sector health

- The split — orders up but output down — points to a supply/cost constraint, not a demand problem

- If sustained, it complicates the Bank of Ghana’s recent dovish posture

- Fuel-price feed-through threatens the 15-month inflation decline streak

What To Watch

- Whether the input-cost rise is a one-off or the start of a trend

- Cedi stability versus the dollar through May

- Energy regulator pricing decisions for the next bi-weekly window

- Manufacturing-sector specific PMIs for confirmation

Follow Vibes Uncut Media for continuing Ghana macro coverage.

Leave a Reply